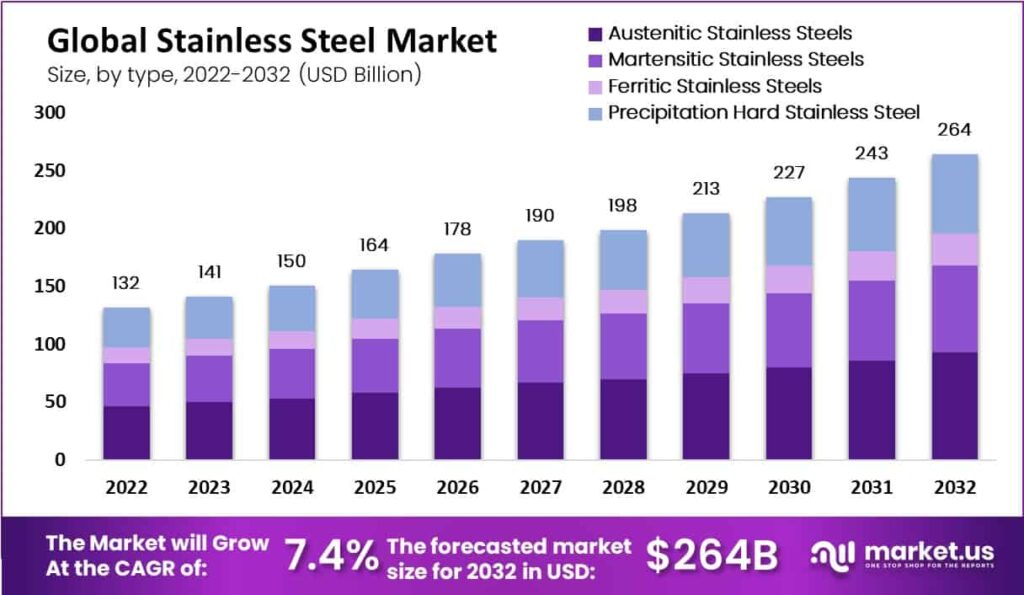

According to Market.us, The Global Stainless Steel Market size is expected to be worth around USD 264 billion by 2033 from USD 131.5 billion in 2023, growing at a CAGR of 7.4% during the forecast period 2023 to 2033.

Stainless steel, an alloy containing 10-30% chromium, is enhanced with elements like nickel, molybdenum, and others to boost oxidation resistance and corrosion resistance, affording it unique properties. This steel is refined in electric arc or basic oxygen furnaces and polished using argon-oxygen decarburization to lower carbon content. The increasing investment in residential housing and infrastructure is expected to drive the demand for stainless steel. Predominantly used in infrastructure, automotive, construction, and various industrial sectors, stainless steel offers significant advantages over carbon steel, including durability, aesthetic appeal, and low maintenance costs. These factors are anticipated to fuel the market’s growth for stainless steel.

Key Takeaway

- The Global Stainless Steel Market size is expected to be worth around USD 264 billion by 2033 from USD 131.5 billion in 2023, growing at a CAGR of 7.4% during the forecast period 2023 to 2033.

- Austenitic stainless steel leads due to its durability, aesthetics, and versatile applications.

- Stainless steel dominates automotive applications, enhancing lightweight design and durability across industries.

- Duplex stainless steel dominates due to its strength and corrosion resistance.

- Asia Pacific dominates with 45%, driving global stainless steel growth.

Factors affecting the growth of the Stainless Steel Market

- Industrial Growth and Urbanization: Increased industrial activities and urbanization in emerging economies are driving the demand for stainless steel. It is extensively used in construction, automotive, and manufacturing due to its durability and resistance to corrosion.

- Innovations and Advancements: Technological advancements in production processes have enhanced the quality and reduced the cost of stainless steel, making it more accessible for various applications. Innovations such as lightweight stainless steel and high-strength compositions are expanding their usage in sectors like automotive, where weight reduction is crucial.

- Regulatory Policies: Environmental and trade regulations can significantly impact the stainless steel industry. Stringent environmental standards encouraging the use of sustainable materials can boost the demand for stainless steel, considered a recyclable and environmentally friendly material.

- Infrastructure Projects: The global emphasis on infrastructure development, including transport networks, bridges, and airports, is a strong growth driver. Stainless steel is favored for its strength and minimal maintenance requirements.

- Economic Conditions: The health of the global economy influences demand for stainless steel. Economic downturns can lead to reduced spending on infrastructure and construction, while economic booms can enhance market growth.

- Supply Chain Dynamics: Fluctuations in the supply of raw materials such as nickel, chromium, and iron, which are integral to stainless steel production, can impact prices and availability of stainless steel.

Top Trends in the Global Stainless Steel Market

- Growth in Consumer Goods and Construction: The consumer goods segment, including products like appliances and utensils, is a major driver due to the material’s corrosion resistance and aesthetic appeal. Similarly, the construction sector is seeing a rebound, particularly in markets that are recovering from the initial impacts of the COVID-19 pandemic, with increased demand for stainless steel in both structural applications and design elements.

- Technological Advancements and Sustainability: Major companies are focusing on technological advancements and sustainability. For instance, some are developing low-carbon footprints for their stainless steel products, which aligns with global pushes toward more sustainable manufacturing practices.

- Market Consolidation and Expansion: The market is witnessing consolidation with major players like ArcelorMittal, Nippon Steel, and Jindal Stainless leading through strategic acquisitions and expansion efforts to enhance their market position and product offerings

- Innovations in Product Applications: There is an ongoing innovation in product applications, particularly in high-performance alloys, which are critical for advanced industrial applications. Companies are actively expanding their capabilities in this area to cater to sophisticated demands from the aerospace, automotive, and energy sectors.

- Impact of Economic Policies and Investments: Economic policies and government investments, particularly in infrastructure, are significantly impacting market growth. For example, government-led initiatives in regions like China and India are boosting local consumption and production through substantial infrastructure projects.

Market Growth

The stainless steel market is experiencing substantial growth, driven by rising demand across various sectors such as construction, automotive, and consumer goods. The market’s expansion is fueled by stainless steel’s advantageous properties, including corrosion resistance, strength, and aesthetic appeal. Innovations in alloy composition and processing technologies are also contributing to market expansion, enabling new applications in harsh environments. Additionally, the increasing emphasis on sustainability is pushing the demand for recyclable and durable materials like stainless steel.

Regional Analysis

The Asia Pacific stainless steel market, holding a dominant 45% share, is expected to see significant revenue growth driven by increased demand in sectors such as chemicals, medical supplies, energy, consumer goods, and transportation, with China leading the region. Europe’s growth is fueled by its automotive industry and technological advancements, while North America benefits from enhanced R&D and technology uptake, particularly in duplex stainless steel for electronics and engineering. In South America, Brazil and Mexico lead, whereas construction booms in the Middle East and Africa are set to propel market expansion in these regions.

Scope of the Report

| Report Attributes | Details |

| Market Value (2023) | USD 131.5 Billion |

| Forecast Revenue (2033) | USD 264 Billion |

| CAGR (2024 to 2033) | 7.4% |

| Asia Pacific Market Share | 45% |

| Base Year | 2023 |

| Historic Period | 2020 to 2022 |

| Forecast Year | 2024 to 2033 |

Market Drivers

The expansion of the stainless steel market is predominantly driven by its extensive utilization across diverse industries including construction, automotive, and consumer goods due to its corrosion resistance, durability, and aesthetic appeal. Increasing urbanization and industrialization, particularly in emerging economies, are catalyzing the demand for infrastructure and transportation solutions, thereby propelling stainless steel consumption.

Additionally, advancements in steelmaking technologies that enhance production efficiency and environmental sustainability further bolster the market growth. Regulatory pressures and rising consumer awareness regarding environmentally sustainable materials are also pushing industries toward stainless steel, viewed as a recyclable and green alternative. These factors collectively underpin the robust growth trajectory of the stainless steel market.

Market Restraints

The stainless steel market faces several restraints that can impact its growth trajectory. One significant limitation is the volatility of raw material prices, particularly nickel, chromium, and iron, which are essential for stainless steel production. Such price fluctuations can lead to inconsistent supply chains and affect production costs.

Additionally, the market is challenged by stringent environmental regulations concerning the production processes, which often involve high energy consumption and CO2 emissions. These regulations increase operational costs and compel manufacturers to invest in cleaner, albeit more expensive, technologies. Furthermore, competition from substitute materials like aluminum and composite materials, which offer similar benefits at potentially lower costs, also poses a threat to the stainless steel industry.

Opportunities

The global demand for stainless steel is expected to surge, driven by escalating infrastructure initiatives and development across nations. Historically, the consumption of steel has been influenced by a myriad of factors such as structural inadequacies, political instability, and fluctuating financial markets. The anticipated growth in steel demand is poised to potentially surpass predictions in the coming years, fueled by globalization, heightened consumer expectations, and rising disposable incomes worldwide. This surge presents significant opportunities within the stainless steel industry.

However, whether the industry can adequately meet this burgeoning demand remains uncertain, underscoring the need for strategic planning and investment in production capabilities.

Report Segmentation of the Stainless Steel Market

By Type Analysis

Austenitic stainless steel, known for its strength, durability, and corrosion resistance, dominates the stainless steel market. It’s aesthetically pleasing, easy to manufacture, and maintain, and environmentally friendly, making it a top choice for architectural and automotive components. Martensitic stainless steel, also corrosion-resistant, offers excellent strength. Ferritic stainless steel, a non-hardening alloy, contains 10.5% to 30% chromium and less than 0.20% carbon, hardening only slightly upon cold rolling. Precipitation-hardened stainless steel features corrosion resistance, while duplex stainless steel blends the qualities of ferritic and austenitic types.

By Application Analysis

The automotive and transportation sector dominates stainless steel applications, recognized for enhancing vehicle light-weighting. This contrasts with historical reliance on costlier light metals. Stainless steel’s superior mechanical properties, coupled with its exceptional weldability and formability, empower designers to create lighter, robust components. Beyond automotive uses, stainless steel is integral in construction, recognized for over a century for its attractiveness, corrosion resistance, and maintenance ease. Its durability and strength are also vital in heavy industries like steel production, mining, and energy sectors, which depend on robust materials for large-scale operations.

By Grades Analysis

The Duplex series stainless steel leads the market due to its superior properties including high strength, lightweight, and exceptional corrosion resistance, particularly against stress corrosion cracking. This dominance is anticipated to boost demand through 2032. The Duplex stainless steel finds extensive use across various sectors such as pharmaceuticals, oil and gas, water desalination, and chemical and petrochemical industries. Other stainless steel series include the 200, 300, and 400 series, each employed in different applications ranging from automotive to medical tools, but it is the Duplex series that stands out for its robust applications in demanding environments.

Recent Development of the Stainless Steel Market

- Aperam acquired ELG, a global recycler of stainless steel, for a value of USD 358.3 Million.

- VINCO launched a new line of steel wires and slings. These wires have significant applications in the Fishing, industrial, elevation, and lifting sectors.

- ArcelorMittal stainless steel company agreed to acquire an 80% interest in Voestalpine’s well-known Hot Briquetted Iron (“HBI”) located in Corpus Christi, Texas.

Competitive Landscape

In the global stainless steel market, Acerinox S.A., Aperam Stainless Steel, and ArcelorMittal represent key players, each holding significant market shares due to their expansive production capacities and extensive geographic presence. Companies like Baosteel Group and Nippon Steel Corporation continue to innovate within the industry, focusing on high-grade stainless steel products that meet increasing environmental standards and regulatory requirements. Jindal Stainless and Outokumpu are noted for their strategic investments in technology to improve operational efficiencies and cost-effectiveness, which are crucial for maintaining competitive edges.

POSCO and Yieh United Steel Corporation are making strides in integrating vertical operations, which enhance their supply chain management and response to market fluctuations. ThyssenKrupp Stainless GmbH, AK Steel Corporation, and JFE Steel Corporation are leveraging advanced technologies to produce differentiated products that cater to niche markets, such as automotive and aerospace, which demand specialized materials. The presence of other key players stimulates competition, driving innovations across the board, thereby ensuring the market’s dynamism and sustainability.